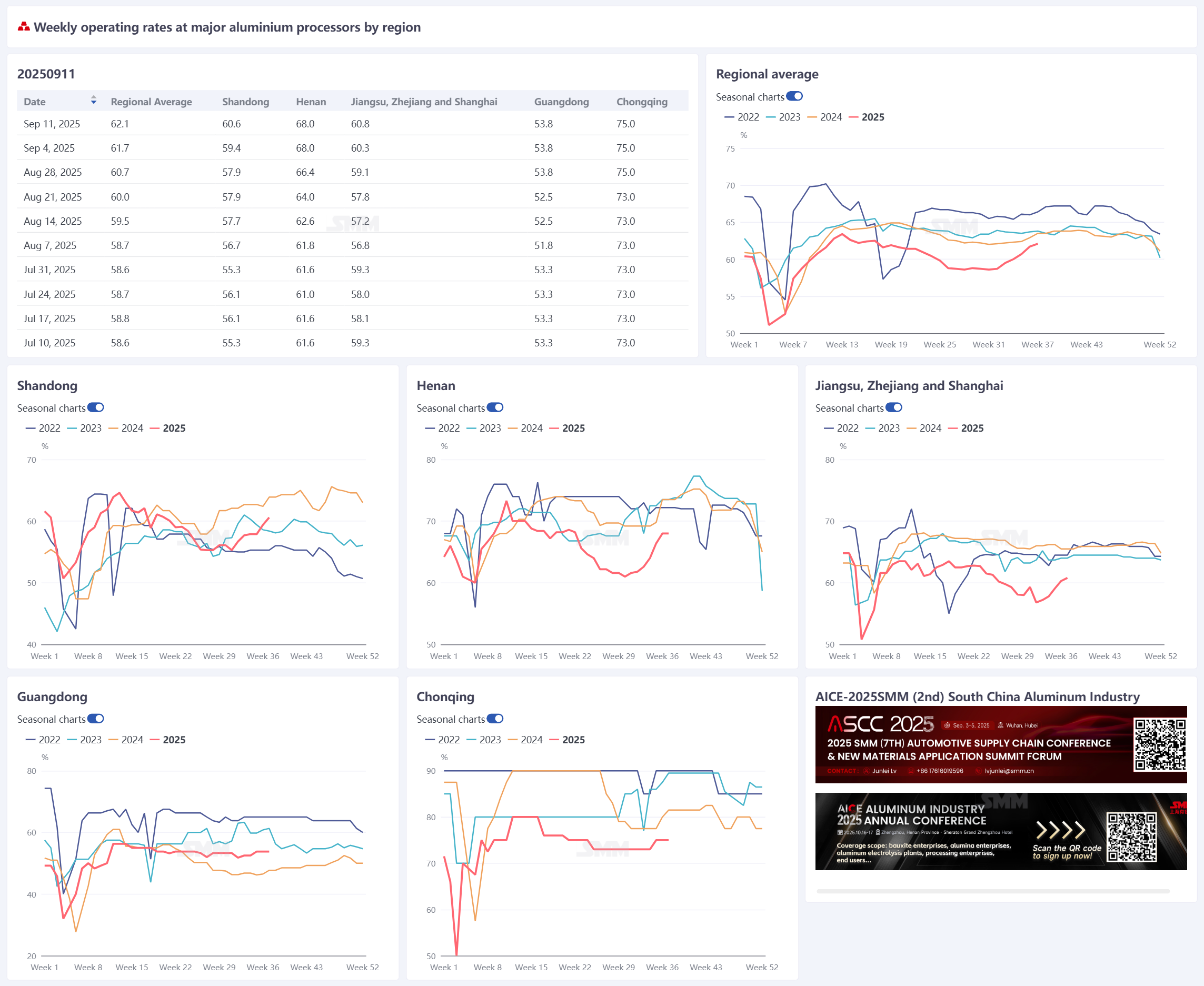

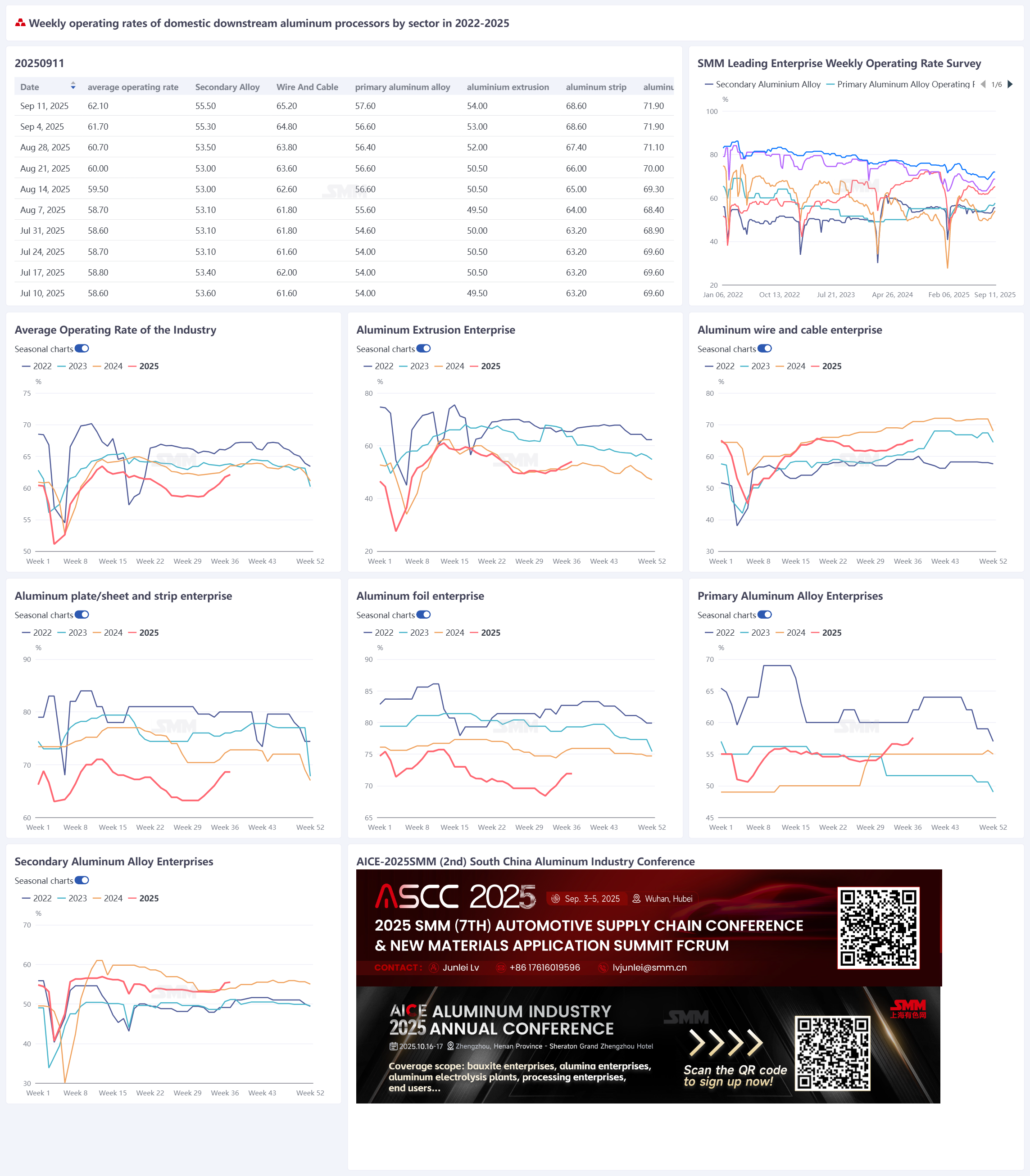

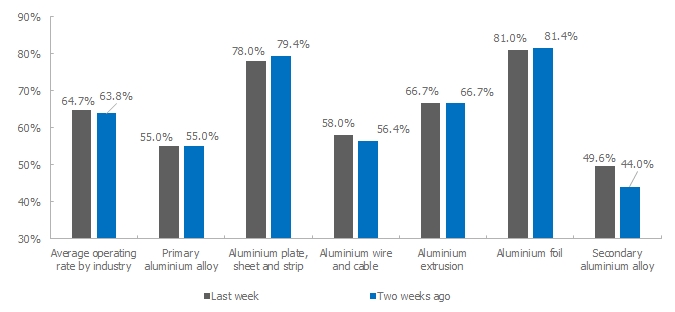

September 12, 2025:

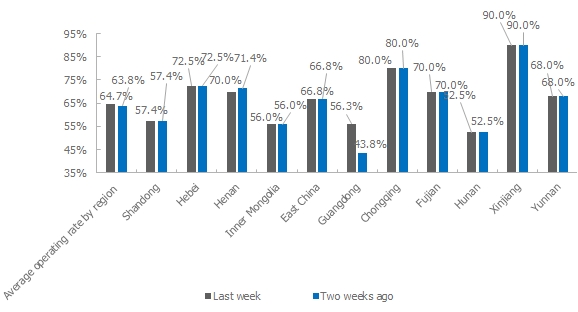

This week, the overall operating rate of leading aluminum downstream processing enterprises in China rose 0.4 percentage points WoW to 62.1%, with the "September peak season" effect continuing to strengthen and various sectors showing a stepwise recovery pattern. The operating rate of the primary aluminum alloy sector increased significantly by 1 percentage point to 57.6%, driven by strong capacity release from top-tier enterprises, though small and medium-sized enterprises still faced order gaps. The aluminum wire and cable industry's operating rate edged up 0.4% to 65.2%, as regional environmental protection inspections were lifted, but capacity recovery in Hebei lagged behind expectations, while power grid orders supported higher operating rates at leading firms. The aluminum extrusion operating rate rebounded 1 percentage point to 54%, with accelerated transition from architectural to industrial profiles, processing fees for PV frames hitting bottom and stabilizing, and new orders for automotive extrusion becoming a highlight. The operating rate of leading aluminum plate/sheet and strip enterprises held steady at a high of 68.6%, as the can stock stockpiling cycle neared its end, and demand resilience in automotive/3C sectors stood out. The aluminum foil industry's operating rate remained at a peak level of 71.9%, though peak season order growth fell short of expectations, with stable demand for packaging foil and battery foil. The operating rate of secondary aluminum producers rose slightly by 0.5% to 53.5%, as consumption-side improvements drove the rebound, but raw material shortages and policy factors continued to constrain capacity recovery. SMM believes that, driven by consumption recovery in terminal sectors such as 3C, automotive, and PV, the aluminum processing industry has re-entered its peak season rhythm. Although the real estate sector remains sluggish, ongoing order releases in the new energy sector have effectively offset this, and downstream aluminum consumption is still expected to increase. SMM expects the operating rate of the aluminum processing industry to continue rising in mid-September, but cautions about the impact of high aluminum prices on downstream stocking willingness.

Primary alloy: Entering the second week of September, the primary aluminum alloy sector's operating pace showed a steady upward trend, with the operating rate rising another 1 percentage point WoW to 57.6%, as industry capacity release strengthened compared to the first week, and some enterprises significantly boosted production enthusiasm. From actual enterprise operations, some firms reported a notable WoW increase in primary aluminum usage this week, while others feedback indicated a roughly 10% rise in early September operating levels compared to earlier periods, with peak season capacity utilization rates continuing to climb; simultaneously, some enterprises have clear expectations for overall September growth, with subsequent expansion intentions reflected in production planning. By scale, top-tier and large-scale enterprises, leveraging stable order reserves and mature supply chains, maintained consistent capacity release, with primary aluminum procurement and consumption volumes staying high, serving as the core force driving the sector's operating rate higher; though small and medium-sized enterprises were buoyed by the overall market sentiment and saw improved operating willingness, some still faced issues with order instability, downstream procurement pace not fully synchronizing, and actual capacity release lagging behind top-tier firms, requiring further observation of the recovery rhythm. As the peak season deepens, SMM expects the primary alloy industry's operating performance to continue strengthening. Aluminum Plate/Sheet and Strip: The operating rate of leading enterprises in the aluminum plate/sheet and strip sector recorded 68.6% this week. Aluminum prices continued to rise during the week, with spot aluminum approaching the 21,900 yuan mark, reigniting downstream fear of high prices. As the mid-September peak season approaches, market trading sentiment has recovered somewhat, but product performance has diverged significantly. Demand for aluminum plate/sheet and strip from industries such as automotive and 3C remains steadily supportive. Can stock producers reported that stockpiling orders for the Mid-Autumn Festival and National Day period have been largely completed, and production schedules are gradually showing weakness, with an order gap of 10-20% YoY. Overall, if aluminum prices continue to fluctuate at highs and break through the 21,000 yuan mark, it may further suppress downstream order placement and cargo pick-up enthusiasm. Without a significant climb in downstream consumption, this will impact enterprise operating rates. It is expected that the operating rate of leading aluminum plate/sheet and strip enterprises will remain stable or experience a slight rise in the short term.

Aluminum Wire and Cable: The operating rate in the aluminum wire and cable industry increased slightly by 0.4 percentage points to 65.2% this week, with leading enterprises showing stable and slightly improved production performance. By region, in Hebei, as environmental protection monitoring for the September 3rd military parade ended, producers gradually resumed operations. However, due to differences in order delivery cycles, the overall operating level did not rebound significantly. From the investment side, the State Grid completed cumulative investments of 270 billion yuan in H1, up 11.7% YoY, but this accounted for less than 50% of the annual plan. Market expectations are strong for investment release in H2 driven by the fourth batch of ultra-high voltage (UHV) tenders. Regarding tender progress, four batches of power transmission and transformation and three batches of UHV tenders have been completed. The pace of power transmission and transformation tenders met expectations, while UHV tenders were slightly below the plan at the beginning of the year. It is expected that the remaining two batches of power transmission and transformation and three batches of UHV tenders will be completed in Q3 and Q4. The industry is currently in a transition phase of "strong expectations, weak reality." Although tendering accelerated in H1, end-user cargo pick-up has not significantly strengthened. SMM expects the operating rate to remain stable at around 65% next week.

Aluminum Extrusion: The operating rate of leading domestic aluminum extrusion enterprises rebounded by 1 percentage point MoM to 54% this week. With the arrival of the September peak consumption season, most extrusion enterprises reported improved order situations. It is understood that some medium and large enterprises in Anhui and Shandong are advancing the phase-out and replacement of outdated capacity, which is expected to further increase capacity concentration and provide some support to the overall industry operating rate. From segmented sectors: In architectural extrusion, affected by the continued weakness in the real estate market, new orders in the industry are generally weak, with production mainly relying on orders on hand, leading to sluggish growth in operating rates. Against this backdrop, some small and medium enterprises in Jiangsu and Anhui reported attempting to adjust production layouts to shift into the industrial extrusion field or explore overseas markets for breakthroughs. Meanwhile, some medium and large enterprises in Guangdong and Shandong reported that architectural extrusion still dominates their capacity, mainly because industrial extrusion requires higher technical standards, has relatively lower yield rates, and offers limited profit margins. In industrial extrusion, PV extrusion operations remain stable, with processing fees for PV frames tending to stabilize recently. A large PV frame producer in Anhui stated that its production costs have basically hit bottom, leaving limited room for further compression of processing fees. In automotive extrusion, some enterprises in Anhui, Fujian, and Hebei reported that new orders in battery tray and bumper beam segments performed relatively well, providing some support to operating rates, but a downward trend in industry processing fees has gradually emerged. Overall, the aluminum extrusion industry has shown traditional peak season characteristics in September. However, some enterprises in Guangdong and Fujian reported that current orders on hand can only sustain 7-14 days of production, expressing concerns about the sustainability of subsequent orders. SMM will continue to track the actual fulfillment of orders across various sectors. Aluminum Foil: The operating rate of leading aluminum foil enterprises recorded 71.9% this week. The aluminum foil market remained relatively stable during the week. The current peak season has provided limited overall lift to aluminum foil demand, and the growth rate of enterprise operating rates was not ideal. Demand for products such as packaging foil and battery foil showed no significant changes, and feedback on production schedules for brazing materials indicated no noticeable increase YoY. Overall, in the short term, supported by the peak season, the operating rate of leading aluminum foil enterprises can still maintain a relatively high level. However, downstream end-users, despite being in the peak season, did not provide excess production orders, making the peak season performance less pronounced. Uncertainties persist, and it is expected that the operating rate of leading aluminum foil enterprises will fluctuate upward slightly in the near future.

Secondary Aluminum Alloy: The operating rate of leading secondary aluminum enterprises increased slightly by 0.2 percentage points WoW to 55.5%, mainly driven by improvements on the consumption side. Since September, downstream procurement sentiment has recovered slightly, and demand has continued to rebound, but the actual strength of the traditional peak season remains to be verified. However, the overall recovery in industry operating rates is still constrained by factors such as insufficient raw material supply and policy uncertainties. Tight circulation resources of domestic and imported aluminum scrap, coupled with increased demand from scrap utilization enterprises, have led to a continuous rise in aluminum scrap prices. Some enterprises, to ensure order delivery, had to purchase at high prices or even across regions. To avoid losses, manufacturers have become more cautious in taking orders, actively controlling order scale and operating levels. In the short term, the industry operating rate may continue its mild rebound trend, but raw material shortages and policy factors will continue to constrain the flexibility of capacity recovery.